Fractions is a topic from elementary mathematics but surprisingly even some Ph.Ds in math have problems with them. After this lesson you will be able to read pie diagrams, calculate portfolio weights and weighted average returns. This lesson does not substitute systematic learning but helps you to recall fractions and demonstrates their usage in trading context.

To understand fractions is a non-trivial challenge, I myself had problems with them in the secondary school. Moreover, a prominent mathematician Vladimir Arnold has reported that his Ph.D. students in France did have problems with fractions. Most likely this is because fractions are introduced in a secondary school and a teacher usually gives rules how to manipulate them but does not explain the motivation behind. But the mathematical genius Henri Poincaré used to say: it is impossible to master the fractions without (mentally) cutting up an apple or a pie.

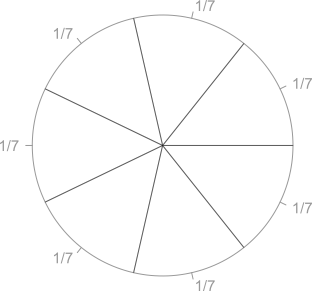

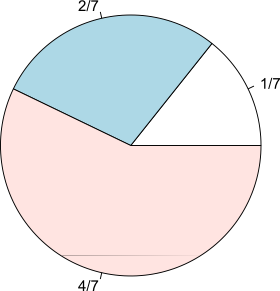

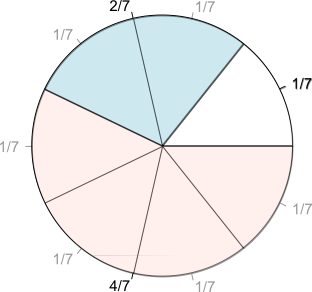

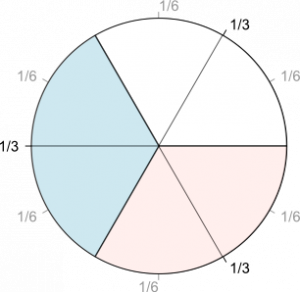

Let us first (equally) share a pie among seven friends. Had we seven pies the operation would be elementary:

a  |

b  |

c  |

|

| Figure 1: a) equally sharing a pie in 7 parts b) non-equal shares with (common) denominator 7 c) a hint how to add fractions with common denominator |

|

A little bit more complicated case is a non-equal pie sharing. A "pie" may be e.g. the initial capital of a firm: if the first partner invests $10000, the second invests $20000 and the third one invests $40000 then the total capital is

Now you also (should) easily understand how to multiply fractions: once again, a fraction is a directive to divide, hence

Example 1: if you invest

In Example 1 you have also seen how we can convert between common and decimal fractions. In order to convert to a decimal fraction you need to obtain 10, 100, 1000, etc in denominator by multiplying or dividing both denominator and numerator by a common factor. Finding this factor may be a little bit challenging, e.g

As to division by a fraction, it is less intuitive (indeed, dividing a pie among "one half" or "two thirds" persons hardly makes sense). But as a mathematical operation it is not uncommon and can be easily formalized:

The last rule we need to understand is how to add the fractions with different denominators.

|

|

|

| Figure 2: bringing fractions to a common denominator | |

In order to add

Bringing to a common factor essentially means further (finer) division (or better to say split), as Figure 2 shows. For example, in order to sum

Sometimes

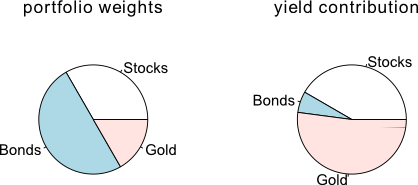

Finally, let us apply our skill to a task from portfolio management.

Assume a financial (robo) advisor tells you that you should invest

Further assume that the stocks grew by 20%, the bonds gave you 2% of return and the gold grew by 50%. So what is the average return on your investments (or in other words, what is the total return of your portfolio)?!

A naive (innumerate) investor would probably state it is (20% + 2% + 50%) / 3 = 24%. This is, however, wrong. It would be correct if the shares (=weights) of all assets were equal. But generally they are not and we have to calculate the weighted average as follows:

Let's check the correctness of our approach with some concrete numbers. Assume (for computational simplicity) that the initial capital was $60000.

So we put $20000 in stocks, $30000 in bonds and $10000 in gold. These investments, respectively, yielded 20% * $20000 = $4000, 2% * $30000 = $600 and 50% * $10000 = $5000. Total gain in $4000 + $600 + $5000 = $9600. And 9600 / 60000 = 0.16 = 16%, as expected.

Finally, let us visualize our computations by means of the pie diagrams

To create Figure 3 I used the following R-code:

#Left-hand pie diagram (initial portfolio weights)

par(mfrow=c(1,2)) #split panel in two (left-right)

slices <- c(1/3, 1/2, 1/6)

lbls <- c("Stocks", "Bonds", "Gold")

pie(slices, labels = lbls, main="portfolio weights")

#right-hand pie diagram (yield contribution)

slices <- c((1/3 * 0.2), (1/2 * 0.02), (1/6 * 0.5))

lbls <- c("Stocks", "Bonds", "Gold")

pie(slices, labels = lbls, main="yield contribution")

Note, however, that the application of the pie diagrams is limited. They are very convenient when you have to visualize the size of shares of a unit, of something holistic. But if some assets had brought a negative return, it would be impossible to use the pie diagram because we cannot visualize negative numbers on them. Moreover, if a unit consists of many parts and some of them have small weights, they may become hardly visible. Thus I, for one, usually prefer the bar plots.

FinViz - an advanced stock screener (both for technical and fundamental traders)