In our previous post on Nelson-Siegel model we have shown some pitfalls of it. In this follow-up we will discuss how to circumvent them and how machine learning and artificial intelligence can[not] help. Continue reading "Pitfalls of Nelson-Siegel Yield Curve Modeling – Part II – what ML and AI can[not] do"

Category: FixedIncome

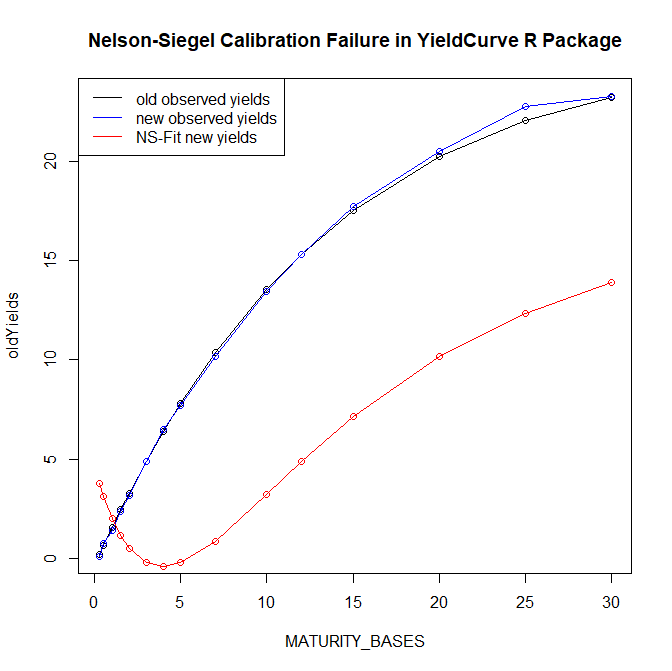

Pitfalls of Nelson-Siegel Yield Curve Modeling – Part I

The Nelson-Siegel-[Svensson] Model is a common approach to fit a yield curve. Its popularity might be explained with economic interpretability of its parameters but most likely it is because the European Central Bank uses it. However, what may do for ECB will not necessarily work in all cases: the model parameters are sometimes extremely unstable and fail to converge. Continue reading "Pitfalls of Nelson-Siegel Yield Curve Modeling – Part I"

Continue reading "Pitfalls of Nelson-Siegel Yield Curve Modeling – Part I"

Zinsen gibt es: in der USA

In Deutschland gibt es seit Jahren keine [Anlage-]Zinsen. In EU-Raum bieten zwar die langfristigen Spanischen oder Italienischen Staatsanleihen ca. 3% Rendite an (und die Griechen versprechen sogar ca. 5%), ist diese Risikoprämie wohl nicht umsonst. Darüber hinaus gibt es nicht für jedes EU-Land entsprechenden Anleihen-ETF, auf jeden Fall nicht unter gebührenfreien ETFs von DeGiro.

Gleichzeitig bietet die USA langfristig fast 3% p.a. an und man kann mittels iShares 20+ Year Treasury Bond ETF (ticker TLT) einfach (und durch DeGiro sogar gebührenfrei) investieren. Die Währungsrisiken betrachten wir bei jetzigem Dollarkurs eher als Währungschancen. Die von Fed angekündigte Zinserhöhung ist wohl schon im Kurs berücksichtigt. Continue reading "Zinsen gibt es: in der USA"

Continue reading "Zinsen gibt es: in der USA"