Scalable Capital, made-in-Germany Robo-Advisor, schafft es (mehr als) eine Milliarde Kapital zu sammeln. Wir sehen dahinter ein außergewöhnlicher StartUp-Erfolg und gewöhnliches Scheitern der Investment-Kultur in Deutschland. Continue reading "Scalable Capital durchbricht Milliardengrenze – Erfolg des StartUps und Scheitern des Volkes"

Category: RoboAdvisors

Scalable Capital – ethischer Robo-Advisor made in Germany

Robo-Advisors sind meistens nicht transparent und basieren sich auf in der Praxis nicht funktionierende Modelle wie Markowitz oder Black-Litterman. Darüber haben wir schon sowohl in kurzem Pamphlet "Anti-Asimov’s Three Laws of Robo-Advisory" als auch in fachlichem Artikel "Stripping down the robo-advisors: sparrow-brains inside" berichtet. Anders ist scalable.capital. Scalable legt sein Modell offen und habt u.a. ein ausführliches Whitepaper veröffentlicht. Nach der Besprechung dieses Whitepapers mit Prof. Dr. Stefan Mittnik kann man eindeutig sagen: Scalable schafft den Mehrwert für Investoren. Ob dabei das Leistung/Gebühren Verhältnis passt, muss jeder für sich selbst entscheiden.

Robo-Advisors sind meistens nicht transparent und basieren sich auf in der Praxis nicht funktionierende Modelle wie Markowitz oder Black-Litterman. Darüber haben wir schon sowohl in kurzem Pamphlet "Anti-Asimov’s Three Laws of Robo-Advisory" als auch in fachlichem Artikel "Stripping down the robo-advisors: sparrow-brains inside" berichtet. Anders ist scalable.capital. Scalable legt sein Modell offen und habt u.a. ein ausführliches Whitepaper veröffentlicht. Nach der Besprechung dieses Whitepapers mit Prof. Dr. Stefan Mittnik kann man eindeutig sagen: Scalable schafft den Mehrwert für Investoren. Ob dabei das Leistung/Gebühren Verhältnis passt, muss jeder für sich selbst entscheiden.

Continue reading "Scalable Capital – ethischer Robo-Advisor made in Germany"

Anti-Asimov’s Three Laws of Robo-Advisory

- Falsely affirm that nobody can beat the market

- Substitute the idea of wealth maximization with the idea of cutting-off the management fees.

- Don't disclose anything about the underling portfolio optimization model and avoid showing possible future portfolio dynamics.

Continue reading "Anti-Asimov’s Three Laws of Robo-Advisory"

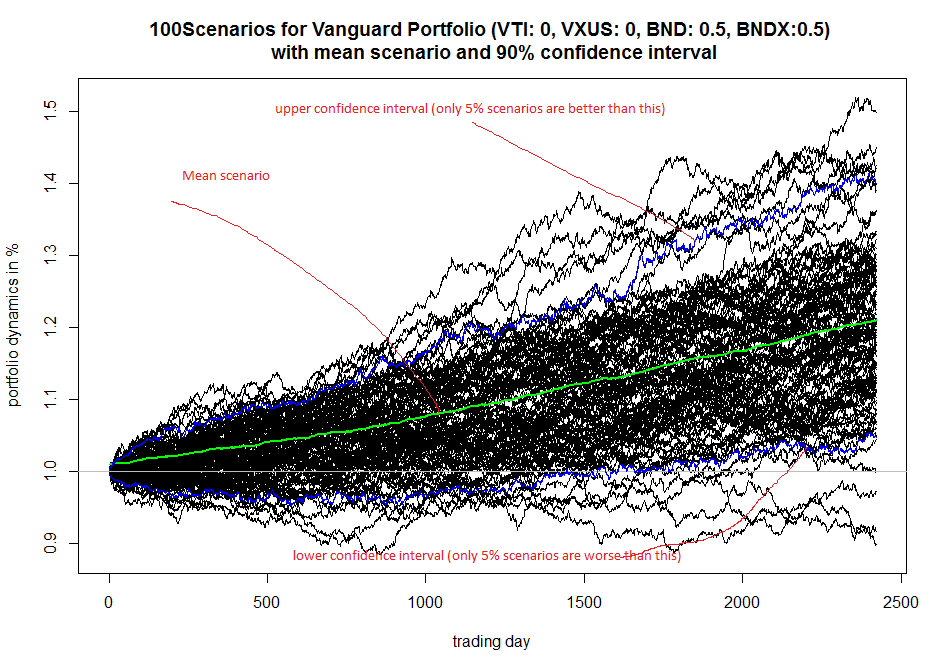

A simple scenario simulator for Vanguard optimal portfolio

There is yet another Roboadvisor from Vanguard Group. As any RoboAdvisor, its recommendations are far from perfection. However, I like it (at least more than others) because the Vanguard guys managed to make it simple. On the other hand I am quite disappointed that they do not show how a suggested portfolio may evolve (and I am quite sure that legendary John Bogle would be disappointed too). That's why I made a simple scenario simulator on my own. It is based on sample with replacement.

There is yet another Roboadvisor from Vanguard Group. As any RoboAdvisor, its recommendations are far from perfection. However, I like it (at least more than others) because the Vanguard guys managed to make it simple. On the other hand I am quite disappointed that they do not show how a suggested portfolio may evolve (and I am quite sure that legendary John Bogle would be disappointed too). That's why I made a simple scenario simulator on my own. It is based on sample with replacement.

Continue reading "A simple scenario simulator for Vanguard optimal portfolio"

Stripping down the robo-advisors: sparrow-brains inside

Summary:

- Robo-advisors promise the risk profiling in a few easy steps, which is unrealistic both from mathematical and behavioral points of view.

- The "optimal" portfolios are usually based on Markowitz-like models, which are inapplicable in practice due to their extreme numerical sensitivity to the market parameters estimation errors.

- Robo-advisors lure investors with low management fees but minimizing fees and maximizing the wealth is not the same. Moreover, the compound costs are not so small in the long term.

- A positive side: Robo-advisers do not (yet) foist toxic financial products upon you.

Continue reading "Stripping down the robo-advisors: sparrow-brains inside"