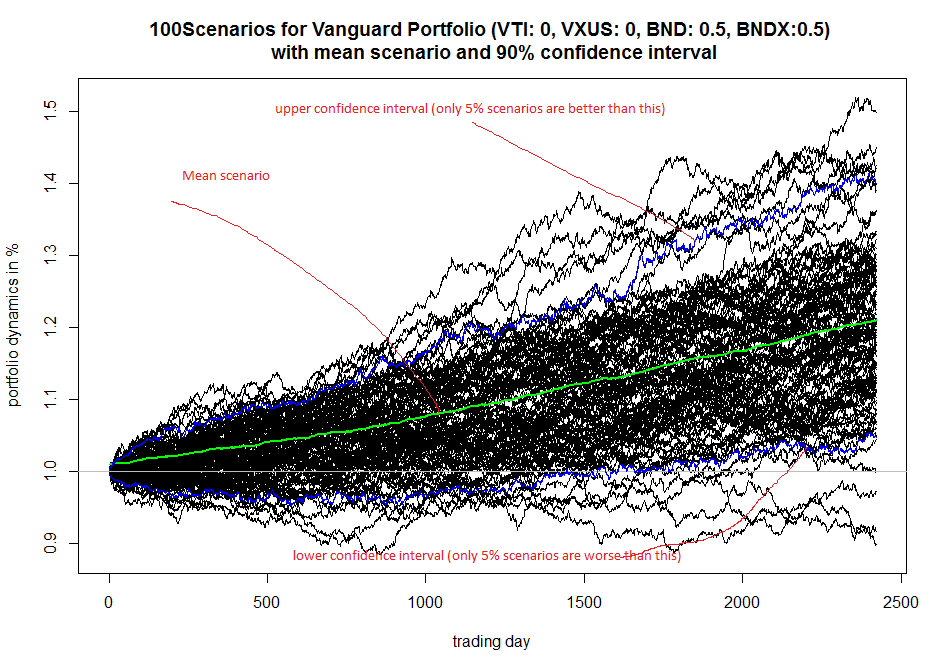

There is yet another Roboadvisor from Vanguard Group. As any RoboAdvisor, its recommendations are far from perfection. However, I like it (at least more than others) because the Vanguard guys managed to make it simple. On the other hand I am quite disappointed that they do not show how a suggested portfolio may evolve (and I am quite sure that legendary John Bogle would be disappointed too). That's why I made a simple scenario simulator on my own. It is based on sample with replacement.

There is yet another Roboadvisor from Vanguard Group. As any RoboAdvisor, its recommendations are far from perfection. However, I like it (at least more than others) because the Vanguard guys managed to make it simple. On the other hand I am quite disappointed that they do not show how a suggested portfolio may evolve (and I am quite sure that legendary John Bogle would be disappointed too). That's why I made a simple scenario simulator on my own. It is based on sample with replacement.

In simple words it means that we randomly select historical daily returns and based on them we construct a future scenario. Then we repeat this approach 100 times and finally calculate the average scenario and the frontiers of 90% confidence interval. This simple simulation is in no way exhaustive but provides some insights on what may happen with your portfolio.

P.S.

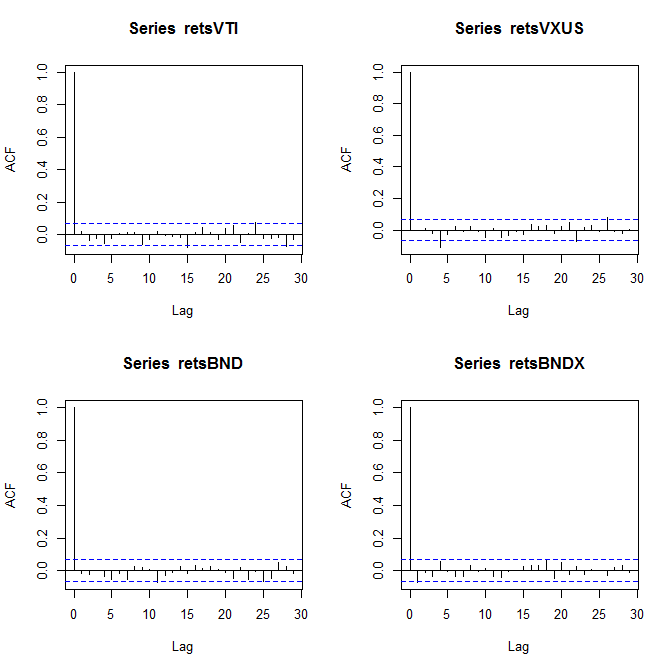

There was a question whether the returns for a given ETF are independent over time (in other words, whether they are serially independent). Yes, they (almost) are! The autocovariances (ACF) are though not exactly zeros but with a few exception are statistically insignificant (i.e. we cannot say for sure that they are not accidental).

As to the correlations between the ETFs, they are of course non zero. Namely they are as follows

| VTI | VXUS | BND | BNDX | |

| VTI | 1.00 | 0.85 | -0.17 | -0.10 |

| VXUS | 1 | -0.10 | -0.11 | |

| BND | 1 | 0.60 | ||

| BNDX | 1 |

We do take them into consideration because we sample the returns tupels for the same date for all funds.

P.P.S.

Vanguard (very briefly) notes the importance of rebalancing. In general, it is the case but here the rebalancing brings nothing! Why?

| VTI | VXUS | BND | BNDX | |

| mean return | 0.000286 | -0.000009 | 0.000002 | 0.00012 |

| volatility | 0.008530 | 0.0102264 | 0.002214 | 0.00198 |

Because the ratios of mean returns and volatilities are such that a portfolio, consisting of VTI only will beat any other portfolio in the long term. You may read my paper for technical details if you like some higher math. By the way, you should invest nothing in VXUS since it has a negative mean return! However, these conclusions follows from historical returns. There is no guarantee that their statistical properties will remain the same in future! That's why it is virtually impossible to calculate the truly optimal portfolios!

FinViz - an advanced stock screener (both for technical and fundamental traders)