After this lesson you will understand how to compute the compound return, discount factors and the CAGR (compound annual growth rate: nominal and inflation adjusted). You will also learn about the continuously compounded (exponential) interest and logarithmic returns. Finally, you will be able to calculate the effective rate of interest of a credit or of a savings scheme.

After this lesson you will understand how to compute the compound return, discount factors and the CAGR (compound annual growth rate: nominal and inflation adjusted). You will also learn about the continuously compounded (exponential) interest and logarithmic returns. Finally, you will be able to calculate the effective rate of interest of a credit or of a savings scheme.

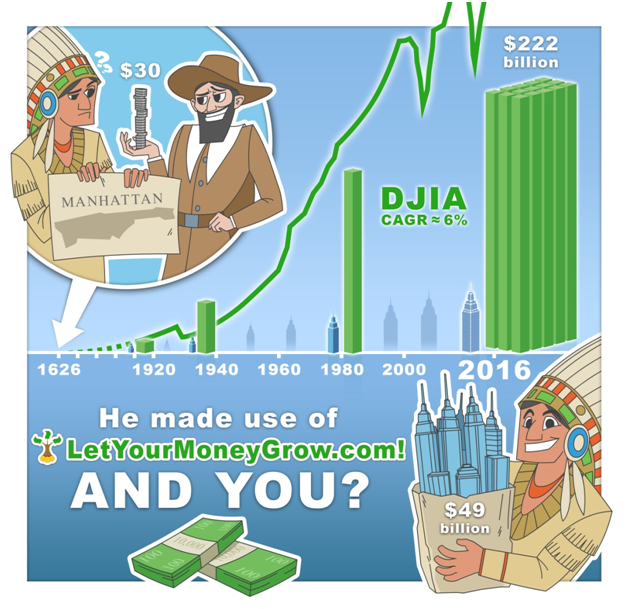

Albert Einstein used to say "Compound interest is the eighth wonder of the world. He who understands it, earns it ... he who doesn't ... pays it". Both parts of his sayings are true and very relevant for every investor. Manhattan was bought for 60 Gulden (about $30) in 1626, which is often considered to be a one of unfairest deals in the history. However, had Native Americans invested this money under 6% per annum (p.a.), they could have bought the Manhattan back with all current real estate four times! Interestingly, the Dow Jones Industrial Average (DJ30) grows approximately 6% p.a. in the long term. Though it is calculated only from 1986, the Amsterdam Stock Exchange was already founded in 1602, so making 6% CAGR since 1926 was, in principle, possible ... at least with a good risk management that would have recognized the tulip mania bubble.

Let us derive a formula to calculate the total yield by the interest rate

Generally, after years your capital is  |

But what if

![K_0 \sqrt[4]{1+r} = K_0 (1+r)^{\frac{1}{4}}](https://s0.wp.com/latex.php?latex=K_0+%5Csqrt%5B4%5D%7B1%2Br%7D+%3D+K_0+%281%2Br%29%5E%7B%5Cfrac%7B1%7D%7B4%7D%7D&bg=ffffff&fg=000&s=0&c=20201002)

Note the following muliplicativity: ![(\sqrt[4]{1+r})^4 = (\sqrt{1+r})^2 = (1+r)](https://s0.wp.com/latex.php?latex=%28%5Csqrt%5B4%5D%7B1%2Br%7D%29%5E4+%3D+%28%5Csqrt%7B1%2Br%7D%29%5E2+%3D+%281%2Br%29&bg=ffffff&fg=000&s=0&c=20201002)

|

There is still a nuance how to calculate the year fraction

Besides the formula

or for a general time of investment : or for a general time of investment :  |

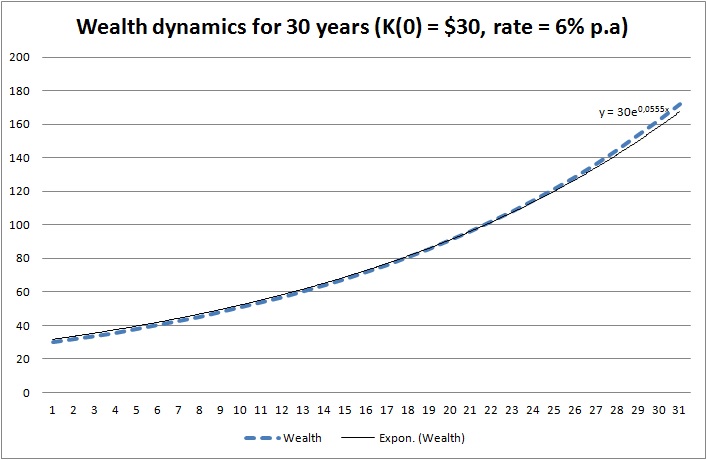

Let us compute the wealth dynamics for the first thirty years under assumption that the Native Americans would put

You see that in 30 years they would get almost the sixfold of the initial capital! But the same is true for a credit: if one borrows $30 and has to pay them back in 30 years, one will pay back $172.30! Think about it every time you take a loan!

You see that in 30 years they would get almost the sixfold of the initial capital! But the same is true for a credit: if one borrows $30 and has to pay them back in 30 years, one will pay back $172.30! Think about it every time you take a loan!

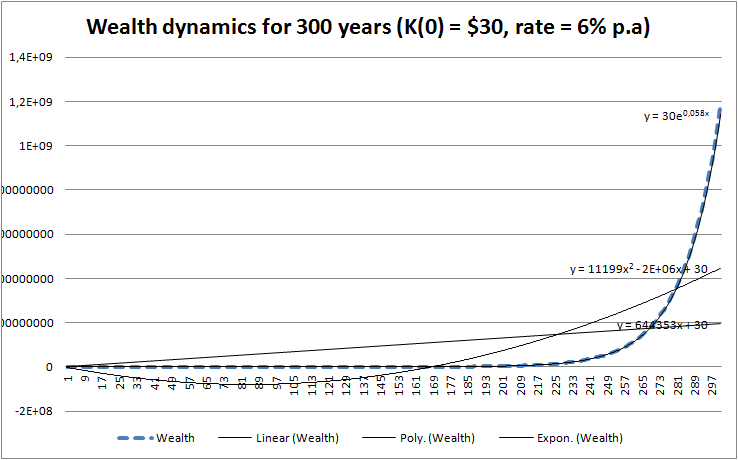

But for the most of people it is difficult to perceive the exponential growth. Such growth does take place in the nature (population growth, powder explosion) but we hardly observe it directly. What we do observe since the stone-age era is a linear function (motion with a constant speed) and a quadratic function (motion with acceleration). But look how the exponential function beats them both over a long term (in this example 300 years)! That's why always calculate your loan costs, don't just rely on your gut feelings, they may let you down in this case!

Let's come back to the interest, compounded according to

Let's come back to the interest, compounded according to

In practice there is virtually no continuously compounded returns but they are ubiquitous in the academic literature and they are very important in order to understand some principle concepts: first of all you readily see that the wealth grows exponentially.

The logarithm is the inverse of the exponential function and in case of continuously compounded rates it is especially easy to calculate the (annualized) return:

It is also common in academic literature to consider the logarithmic returns:

However, since in practice they deal with "normal" compounding, the formula for the annualized return looks a little bit more complicated.

It holds

|

If you have an interest rate, you can also calculate the discount factors. For the continuous rates these are

The inflation is, in a sense, a discount factor. If the inflation rate is

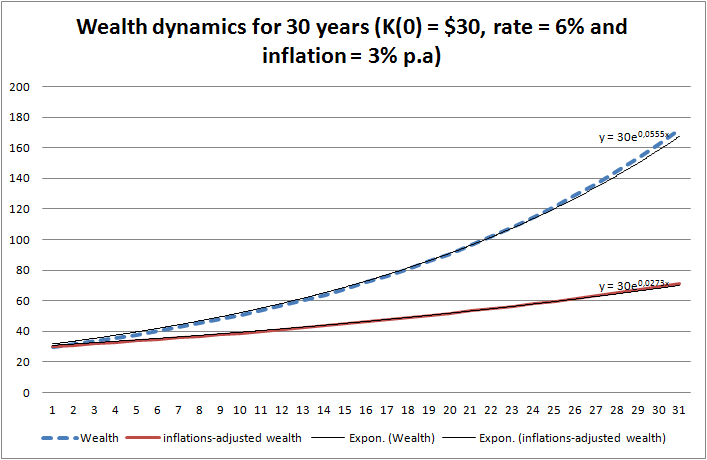

If we consider the inflation

If we consider the inflation

Finally, let us consider the loans and saving plans.

In case of a saving plan one invests (usually monthly) a fixed amount in an ETF. Contrary to the bank deposits, the returns on ETFs are random but for the calculation of the growth rate it doesn't matter much.

Assume that you invest monthly a fixed account

|

Note that for simplicity we assumed the integer number of months and simply divided the (implied) rate

This equation is a polynomial and if

Analogously if you get a loan with a notional amount

|

Note that the monthly installment can be decomposed to the interest you pay to the bank and the debt redemption. The former is bad (it is what the bank earns on you) and the latter is good. We will not explain this decomposition in detail but you can understand it from the Excel sheet, in which we calculated all our examples.

FinViz - an advanced stock screener (both for technical and fundamental traders)