Even if you are not a Forex trader, it is often necessarily to get currency exchange rates, e.g. if you trade [the options on] foreign stocks. Fixer.io provides daily FX-rates from European Central Bank for 31 currencies via JSON API. We present a script to get data in R.

library(jsonlite)

#fetches currency rates w.r.t. EUR for a given date

getFxRatesFromFixerIo = function(refDate)

{

avUrl = paste0("http://api.fixer.io/",refDate)

dat = fromJSON(avUrl)

FX_RATES = array(0.0, dim=c(1,31))

if(!is.null( dat$rates$AUD )) FX_RATES[1] = dat$rates$AUD

if(!is.null( dat$rates$BGN )) FX_RATES[2] = dat$rates$BGN

if(!is.null( dat$rates$BRL )) FX_RATES[3] = dat$rates$BRL

if(!is.null( dat$rates$CAD )) FX_RATES[4] = dat$rates$CAD

if(!is.null( dat$rates$CHF )) FX_RATES[5] = dat$rates$CHF

if(!is.null( dat$rates$CNY )) FX_RATES[6] = dat$rates$CNY

if(!is.null( dat$rates$CZK )) FX_RATES[7] = dat$rates$CZK

if(!is.null( dat$rates$DKK )) FX_RATES[8] = dat$rates$DKK

if(!is.null( dat$rates$GBP )) FX_RATES[9] = dat$rates$GBP

if(!is.null( dat$rates$HKD )) FX_RATES[10] = dat$rates$HKD

if(!is.null( dat$rates$HRK )) FX_RATES[11] = dat$rates$HRK

if(!is.null( dat$rates$HUF )) FX_RATES[12] = dat$rates$HUF

if(!is.null( dat$rates$IDR )) FX_RATES[13] = dat$rates$IDR

if(!is.null( dat$rates$ILS )) FX_RATES[14] = dat$rates$ILS

if(!is.null( dat$rates$INR )) FX_RATES[15] = dat$rates$INR

if(!is.null( dat$rates$JPY )) FX_RATES[16] = dat$rates$JPY

if(!is.null( dat$rates$KRW )) FX_RATES[17] = dat$rates$KRW

if(!is.null( dat$rates$MXN )) FX_RATES[18] = dat$rates$MXN

if(!is.null( dat$rates$MYR )) FX_RATES[19] = dat$rates$MYR

if(!is.null( dat$rates$NOK )) FX_RATES[20] = dat$rates$NOK

if(!is.null( dat$rates$NZD )) FX_RATES[21] = dat$rates$NZD

if(!is.null( dat$rates$PHP )) FX_RATES[22] = dat$rates$PHP

if(!is.null( dat$rates$PLN )) FX_RATES[23] = dat$rates$PLN

if(!is.null( dat$rates$RON )) FX_RATES[24] = dat$rates$RON

if(!is.null( dat$rates$RUB )) FX_RATES[25] = dat$rates$RUB

if(!is.null( dat$rates$SEK )) FX_RATES[26] = dat$rates$SEK

if(!is.null( dat$rates$SGD )) FX_RATES[27] = dat$rates$SGD

if(!is.null( dat$rates$THB )) FX_RATES[28] = dat$rates$THB

if(!is.null( dat$rates$TRY )) FX_RATES[29] = dat$rates$TRY

if(!is.null( dat$rates$USD )) FX_RATES[30] = dat$rates$USD

if(!is.null( dat$rates$ZAR )) FX_RATES[31] = dat$rates$ZAR

return (FX_RATES)

}

attempt = 1

refDate = as.Date('2016-01-03') #min date is 2000-01-03

endDate = Sys.Date()

res = list()

while(refDate <= endDate)

{

possibleError <- tryCatch({

res[[as.character(refDate)]] = getFxRatesFromFixerIo(refDate)

refDate = refDate + 1 },

error = function(err) {

if(attempt > 5) {

print(paste0("Problems with rates on ", as.character(refDate)))

refDate = refDate + 1

attempt = 1

} else {

attempt = attempt + 1

}

})

}

nms = names(res)

N_DAYS = length(nms)

USDts = array(0.0, dim=N_DAYS)

GBPts = array(0.0, dim=N_DAYS)

for(d in 1:N_DAYS)

{

USDts[d] = res[[nms[d]]][30]

}

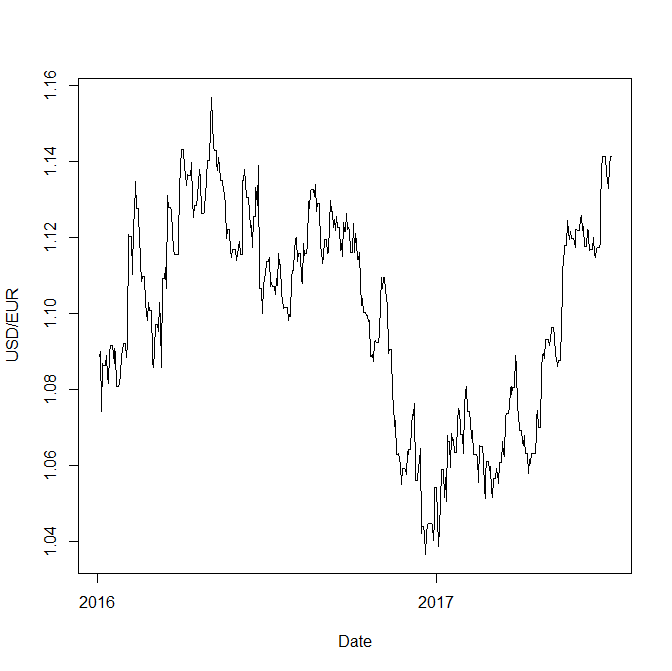

plot(USDts ~ as.Date(nms), type="l",

xlab="Date",ylab="USD/EUR")

The data are available from 2000-01-03, however, not for all currencies. That's why we have to check with is.null(). According to Fixer.io their availability is 99.98%. However, sometimes technical problems do happen. So we need to call getFxRatesFromFixerIo() inside of tryCatch(...). If an error is occurred, we re-send the JSON request upto 5 times.

Like this post and wanna learn more?

Have a look at Knowledge rather than Hope: A Book for Retail Investors and Mathematical Finance Students

FinViz - an advanced stock screener (both for technical and fundamental traders)

FinViz - an advanced stock screener (both for technical and fundamental traders)