Quantopian is a very interesting FinTech project for virtually everybody, who wants to try the algorithmic trading. Yet I explain why I myself - a successful trader, experienced quant and good programmer - don't take part. Continue reading "Quantopian – why I don’t take part"

HSBC “Tradingplan” 2017 – eine Anleitung zum Geldverschwendung – wie Max Mustermann, Beruf Ingenieur sein Geld bei Hobby-Trading verliert

In der Zeitschrift "Marktbeobachtung (Januar 2017)" von HSBC wurde von Jewgeni Ponomarev einen "Tradingplan" für Max Mustermann (Beruf: Ingenieur und Hobby-Trader) veröffentlicht. Wir erklären, warum mit diesem Plan nur die HSBC Bank (auf Kosten von Max Mustermann) das Geld verdient. Continue reading "HSBC “Tradingplan” 2017 – eine Anleitung zum Geldverschwendung – wie Max Mustermann, Beruf Ingenieur sein Geld bei Hobby-Trading verliert"

Book Review: 23 Things They Don’t Tell You About Capitalism

Recently I have read a very interesting book "23 Things They Don't Tell You About Capitalism" by Prof. Ha-Joon Chang. As such it is very interesting and easy going book (no formulas, simple language). But it is much more: in my opinion every investor and trader should read it to better understand the current political and economic trends.

Continue reading "Book Review: 23 Things They Don’t Tell You About Capitalism"

letYourMoneyGrow.com nimmt IndexGarant von SV SparkassenVersicherung unter der Lupe

Aufmerksam darauf gemacht wurde ich durch die Google-Ads hier. Die Werbung versprach attraktive Rendite und dabei keine Verlustrisiken. Das hat meine Forschungsinteresse geweckt. Testergebnis: das Produkt ist innovativ und volle Verlustrisikovermeidung ist möglich. Ob die Rendite aktuell wirklich attraktiv sein wird, ist aber nicht so offensichtlich [UPDATE 20.01.2017 - sie ist nicht attraktiv!].

Aufmerksam darauf gemacht wurde ich durch die Google-Ads hier. Die Werbung versprach attraktive Rendite und dabei keine Verlustrisiken. Das hat meine Forschungsinteresse geweckt. Testergebnis: das Produkt ist innovativ und volle Verlustrisikovermeidung ist möglich. Ob die Rendite aktuell wirklich attraktiv sein wird, ist aber nicht so offensichtlich [UPDATE 20.01.2017 - sie ist nicht attraktiv!].

Deutsche Vermögensverwaltung: unfähige institutionelle Assetmanager und selbsternannte Börsengurus

Während der Zerozinsenzeit wird immer lauter darüber gesprochen, dass man sein Geld lieber investieren als auf Tagesgeldkonto parken sollte. An sich ist es richtig, aber mit der Auswahl des Vermögensverwalters muss man sehr vorsichtig sein. Der bekehrte Schwabe empfielt: schauen Sie selbst die Performance an, anstatt die Werbung blind zu vertrauen. Erinnern Sie sich immer daran, dass die kostenlosen "Beratungsgespräche" fast immer Verkaufsgespreche sind! Eine Alternative dazu ist die Honorarberatung, jedoch ist ein Honorarberater ohne Track Record nichts Wert! Passive Anlage ist generell keine schlechte Idee, aber selbst der Aufbau eines gut diversifizieren Portfolios ist auch keine triviale Aufgabe.

Während der Zerozinsenzeit wird immer lauter darüber gesprochen, dass man sein Geld lieber investieren als auf Tagesgeldkonto parken sollte. An sich ist es richtig, aber mit der Auswahl des Vermögensverwalters muss man sehr vorsichtig sein. Der bekehrte Schwabe empfielt: schauen Sie selbst die Performance an, anstatt die Werbung blind zu vertrauen. Erinnern Sie sich immer daran, dass die kostenlosen "Beratungsgespräche" fast immer Verkaufsgespreche sind! Eine Alternative dazu ist die Honorarberatung, jedoch ist ein Honorarberater ohne Track Record nichts Wert! Passive Anlage ist generell keine schlechte Idee, aber selbst der Aufbau eines gut diversifizieren Portfolios ist auch keine triviale Aufgabe.

7 good Wikifolios – Automatic Statistical Performance and Risk Analysis

Wikifolio is a FinTech start-up that lets virtually everybody to become an fund manager. Wikifolio adheres to highest public disclosure standards, in particular current portfolios and complete trading statistics are available in real time. However, wikifolio lacks any statistical and chart analysis. One cannot even add a benchmark like DAX or DJ30 to a wikifolio chart.

We propose a way to increase the value of disclosed information and looking forward for feedback from both Wikifolio trades and investors. We also hope for official feedback from Wikifolio team.

Continue reading "7 good Wikifolios – Automatic Statistical Performance and Risk Analysis"

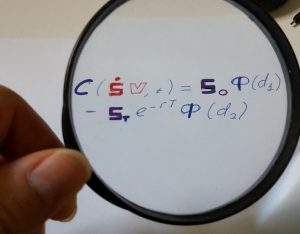

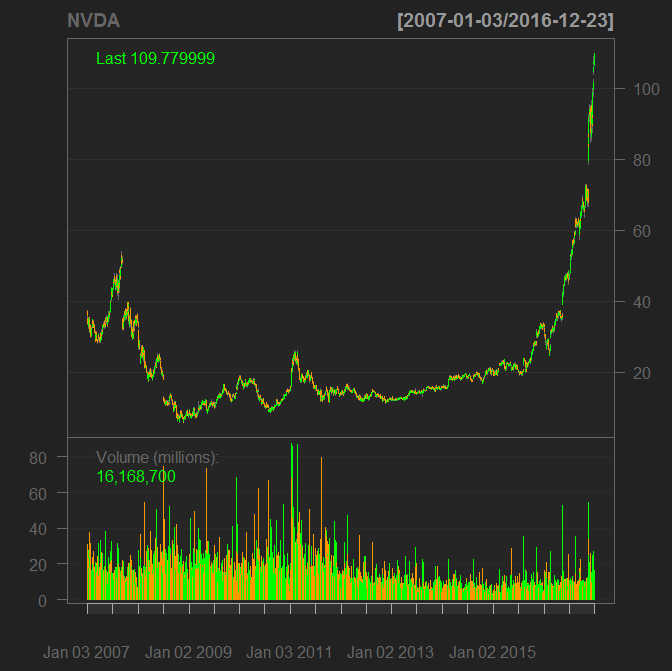

My PUT Option on NVIDIA – a case study of nearly perfect trading decision

NVIDIA stock (NVDA, US67066G1040) has recently exploded. Though the profits also significantly grew, the stock bubble is definitely overproportional to fundamentals. Most likely this is due the deep learning hype. So I bought a put option on NVIDIA and even if it expires worthless, I still consider it as a nearly perfect trade and explain why.

NVIDIA stock (NVDA, US67066G1040) has recently exploded. Though the profits also significantly grew, the stock bubble is definitely overproportional to fundamentals. Most likely this is due the deep learning hype. So I bought a put option on NVIDIA and even if it expires worthless, I still consider it as a nearly perfect trade and explain why.

Continue reading "My PUT Option on NVIDIA – a case study of nearly perfect trading decision"

Why I am skeptical about investing in “global trends”

Investing in a "globaly demanded" product or service seems (at first glance) to be a nice idea. However, it may be (too) dangerous: not all global trends turn into profit and even if they do, you need to get in early since most of global trends (even genuine) turn into bubbles and do burst.

Continue reading "Why I am skeptical about investing in “global trends”"

Pension Savings Calculator for USA based on SSA Actuarial Life Table

Recently we published an essay about the German pension insurance under the title "How the Father State plunders me". As a matter of fact, German pension system is mainly based on a so-called generation solidarity principle: current employers finance current pensioners (and are supposed to be financed by the following generation as they, themselves, retire). It worked well in Bismarck's time but with current longevity and low birthrate the system is not capable anymore! The calculations with German mortality tables shows: were the employers allowed to invest their contributions themselves, they would not be inevitably condemned to the Altersarmut (elderly poverty).

Though Germans have both private pension insurance and Betriebliche Altersvorsorge (similar 401k plans) they are mainly fixed-interest (thus with current rates they even don't cover the inflation). Still they are much more attractive than the compulsory insurance by the state pension fund.

Continue reading "Pension Savings Calculator for USA based on SSA Actuarial Life Table"

Rentenarmut – wie der Vater Staat mich plündert

Alle Angesteller zahlen erhebliche Rentenversicherungsbeiträge. Darüber hinaus wird genauso viel wird vom Arbeitgeber eingezahlt! Trotzdem sieht die erwartete Rente selbst bei Gutverdienern miserabel aus (und selbst sie ist nicht 100% sicher). Grund dafür ist das Generationssolidaritätsprinzip: die Rentner werden von jetzigen Erwerbstätigen finanziert. Leider muss man zugeben: bei jetziger demografischen Entwicklung (Langlebigkeit und Kinderlosigkeit) scheitert die Generationssolidarität! Was jedoch immer gilt ist das Äquivalenzprinzip: Barwert der Rentenbeiträgen sei gleich dem Barwert den Rentenerträgen! Selbst bei extrem niedrigen Zinsen (für welche auch Vaterstaat zu "danken" ist) wäre die Rente nach Äquivalenzprinzip keine Armutsrente!

Continue reading "Rentenarmut – wie der Vater Staat mich plündert"