Seven years ago I tried to reproduce the results of "Foundations of Technical Analysis: Computational Algorithms, Statistical Inference, and Empirical Implementation" by Lo, Mamaysky and Wang with more recent data than they used. Lo et al come to the conclusion that the chart patterns are statistically significant (which does not yet mean their practical usability). My results shows that there is no statistical significance (anymore). Continue reading "Patterns of Technical Analysis – Do They Work?"

Author: Vasily Nekrasov

Founder of letYourMoneyGrow.com

Quirin Honorarberatung: gut gedacht aber schlecht gemacht

Etablierung der unabhängigen (und deswegen entgeltlichen) Finanzberatung, sowie die transparente und nachvollziehbare Vermögensverwaltung wäre ein großer Vorschritt für die Deutsche Finanzindustrie. Das strebt anscheinend die Quirin Bank. Doch gibt es einige wesentlichen Unterschiede zwischen der Werbung, dem roten Buch von Quirin und der Tatsache. Continue reading "Quirin Honorarberatung: gut gedacht aber schlecht gemacht"

QuantLibXL – A Curvy Way to fit a Yield Curve

QuantLib is a magnificent library for quantitative finance. But it is also like a gun, heavy enough to shoot your own foot. You might expect that QuantLibXL (a plug-in that provides a subset of QuantLib functionality in Excel) makes your life easier. Unfortunately, it hardly does, as we show in this case study. For an easy and straight way you should better have a look at Deriscope. Continue reading "QuantLibXL – A Curvy Way to fit a Yield Curve"

QuantLib is a magnificent library for quantitative finance. But it is also like a gun, heavy enough to shoot your own foot. You might expect that QuantLibXL (a plug-in that provides a subset of QuantLib functionality in Excel) makes your life easier. Unfortunately, it hardly does, as we show in this case study. For an easy and straight way you should better have a look at Deriscope. Continue reading "QuantLibXL – A Curvy Way to fit a Yield Curve"

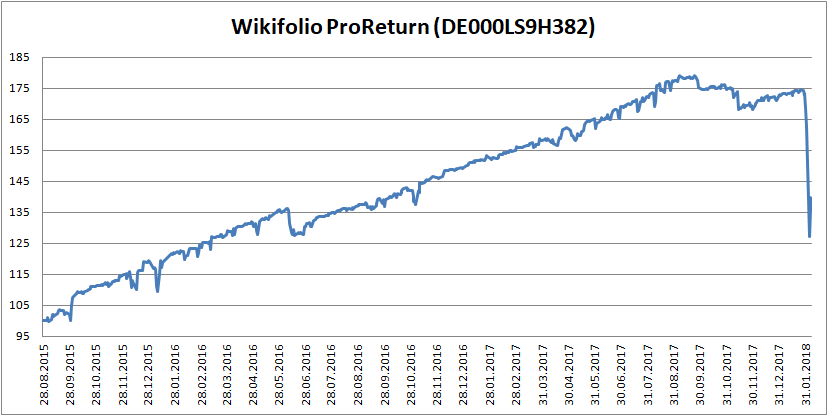

Wikifolio ProReturn is 45% down – Greedy German pays the Price (over and over) again

ProReturn, one of the most popular wikifolios, lost about 45% of its value during recent market flash crash. Several millions Euro disappeared within two days. But it seems that greedy German retail investors will never learn. Moreover, they don't want and are hardly able to learn, although the German school education system is free of charge an still much better than that in US and UK. Well, jedem das Seine!

Continue reading "Wikifolio ProReturn is 45% down – Greedy German pays the Price (over and over) again"

Continue reading "Wikifolio ProReturn is 45% down – Greedy German pays the Price (over and over) again"

Finanzieller Analphabetismus ist auch unter “Profis” keine Ausnahme

Im vorigen Beitrag haben wir krassen Finanz-Analphabetismus in Deutschland erwähnt. Anscheinend herrscht er auch unter den "Profis". Vor kurzem war ich auf einem Kaminabend für "Profis aus Finanzbranche". Es wurde u.a. über Factoring berichtet. Der Typ sagte, Factoring bringt ca. 3% im Monat, so was bringt er per annum? – hat er gefragt. 36% rief man im Chor aus dem Saal. Na ja,

Building QuantLibXL in Visual Studio 2017

QuantLibXL (Excel QuantLibAddin) provides a [limited subset of] QuantLib functionality directly in Excel. However, its development follows the development of QuantLib with a lag, e.g. currently the last modified date in project repository is 2017-05-02. I tried to build QuantLibXL with currently latest version of the Visual Studio (success) and to bind it to the latest version of QuantLib (no way).

Continue reading "Building QuantLibXL in Visual Studio 2017"

FinTech-Days Stuttgart – Schwabenland wacht auf

Baden-Württemberg (und insb. das Schwabenland) ist die reichste Region Deutschlands. Jedoch sind wir im Sinne von FinTech (noch) nicht führend. Dank Stuttgart Financial, Börse Stuttgart, L-Bank, VentureZphere und zahlreiche Sponsors und Teilnehmer holen wir nach. Continue reading "FinTech-Days Stuttgart – Schwabenland wacht auf"

Continue reading "FinTech-Days Stuttgart – Schwabenland wacht auf"

QuantLib for Mere Mortals – Insights from QL User Meeting 2017

We have already used QuantLib at letYourMoneyGrow.com several times, in particular to provide a helpful scenario simulator for option traders. QuantLib User Meeting 2017, in which I also took part, provides insights on how to make QuantLib even more accessible for the "mere mortals".

Continue reading "QuantLib for Mere Mortals – Insights from QL User Meeting 2017"

Rauchen ist tödlich … und macht arm

Es ist generell bekannt, dass das Rauchen die Lebensjahre beraubt. Ich zeige - anhand der Sterblichkeitsstatistik – wie viele. Weniger bewusst ist, wie viel Geld man mit Zigaretten verschwendet (oder besser zu sagen – verraucht). Mit diesem Geld könnte ein Raucher für sein Alter vorsorgen bzw. eine Immobilie finanzieren. Eine schwache Trost für diejenige, die das Rauchen nicht aufgeben können: die Wahrscheinlichkeit, dass Ihr gar keine Altersvorsorge braucht, ist viel höher als bei Nichtraucher.

Continue reading "Rauchen ist tödlich … und macht arm"

Oh This Cranky Sentiment: General Electric vs. Daimler on 20.10.2017

Virtually every trader and investor is aware about technical and fundamental analysis. But little understand the importance of sentiment. We consider a case study of GE vs DAI, which particularly good illustrates the importance and interaction of these three components. Continue reading "Oh This Cranky Sentiment: General Electric vs. Daimler on 20.10.2017"