This is a well-known fact that the stock prices are virtually unpredictable. However, stock volatilities can more or less be forecasted! In 2012 Vasily Nekrasov scrutinized about 3000 asset price time series, obtained from yahoo.finance. Approximately in half of cases the volatility was piecewise-stationary and thus predicatable. We put online the technical record from 2012 and start publishing the visualized results Continue reading "Volatility Clustering and Piecewise Homoscedasticity – Part I – Indices"

Category: AssetAllocation

ETF Sparplan: Risiken und Vorteile richtig verstehen

Wir erklären, wie ein Sparplan funktioniert und warum die Mantra „langfristig wird es nach oben gehen“ für einen ETF-Sparplan ungültig ist.

Continue reading "ETF Sparplan: Risiken und Vorteile richtig verstehen"

Continue reading "ETF Sparplan: Risiken und Vorteile richtig verstehen"

Savings Plan Scenario Simulator

Definitely, you have heard a mantra from many asset managers that want your money: in the long term your investment in stocks or an index ETF will grow. Though for a one-time investment it is generally true (however, not always, recall NIKKEI), it is far away from truth for a savings plan. For instance, even if you run your savings plan for 30 years and assume annually 6% expected return and 20% volatility (very optimistic, indeed), you will make losses in ca. 15% of scenarios. And if your saving plan lasts "only" 10 years, the number of scenarios with losses will be about 30%! Additionally, they delude you showing the mean (or expected) scenario. Mean is highly influenced by a couple of extremely good outcomes: finally, your investment cannot fall below zero but there is no upper bound, at least theoretically. That's why the average scenario often looks too optimistic. It is much better to consider the median as the measure of central tendency instead. Try to simulate your savings plan yourself!

Market Spotlight: Pick up Commodities but be picky

Currently the stocks are expensive and the commodities are cheap (though not all of them). We conduct a lite analysis of investment opportunities and construct a mid-term commodity portfolio for a retail investor with €10000+ capital. Continue reading "Market Spotlight: Pick up Commodities but be picky"

Portfolio Simulator – estimate the expected risk and return of your investments

Our simulator allows you to simulate 100 future scenarios of your portfolios, estimate the expected risk, return and correlations, helping you to improve the diversification of your portfolios. The simulator projects the historical returns in future and is completely model-free (in particular, we don't make an unrealistic assumption of Normally-distributed returns). Though the past doesn't capture all possible future scenarios, it provides a good idea of possible outcomes.

Continue reading "Portfolio Simulator – estimate the expected risk and return of your investments"

Schlechten Tänzer stören immer die eigenen Ho(r)den

Zum 1. April veröffentlicht letYourMoneyGrow.com eine Antwort auf das Interview "Tanzen lernen Sie auch nicht ohne Tanzlehrer" von Marcus Vitt, Vorstandssprechers des Bankhauses Donner & Reuschel. Mit lustigem Titel aber ziemlich ernstem Inhalt.

Continue reading "Schlechten Tänzer stören immer die eigenen Ho(r)den"

Perfect diversification means no asset can be dropped from (rather than added to) a portfolio

A common belief: adding extra asset to a portfolio will automatically reduce the portfolio risk. We provide a counter-example resorting only to the simplest algebra and explain why this erroneous belief is so common.

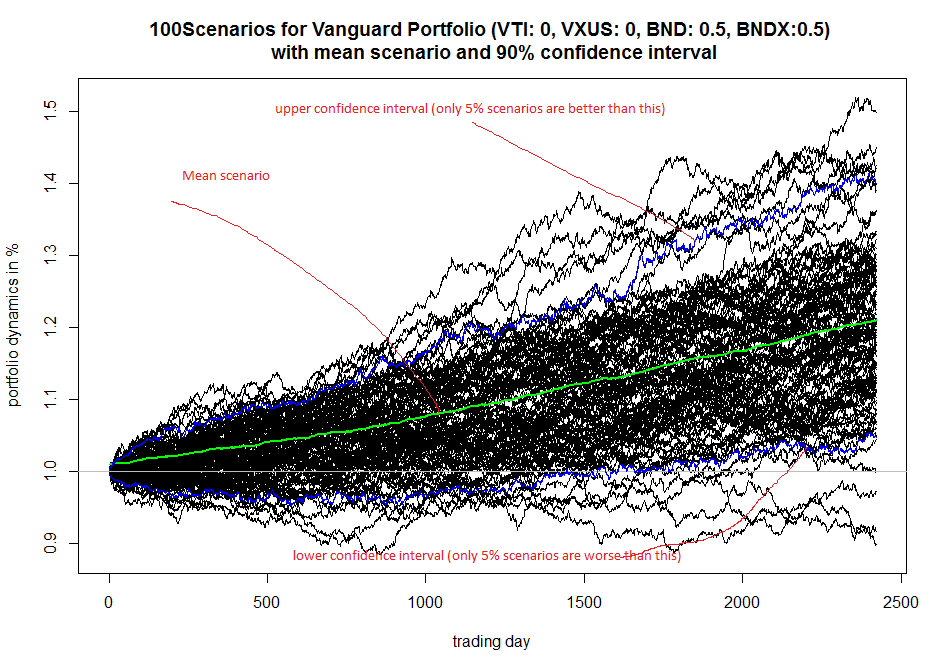

A simple scenario simulator for Vanguard optimal portfolio

There is yet another Roboadvisor from Vanguard Group. As any RoboAdvisor, its recommendations are far from perfection. However, I like it (at least more than others) because the Vanguard guys managed to make it simple. On the other hand I am quite disappointed that they do not show how a suggested portfolio may evolve (and I am quite sure that legendary John Bogle would be disappointed too). That's why I made a simple scenario simulator on my own. It is based on sample with replacement.

There is yet another Roboadvisor from Vanguard Group. As any RoboAdvisor, its recommendations are far from perfection. However, I like it (at least more than others) because the Vanguard guys managed to make it simple. On the other hand I am quite disappointed that they do not show how a suggested portfolio may evolve (and I am quite sure that legendary John Bogle would be disappointed too). That's why I made a simple scenario simulator on my own. It is based on sample with replacement.

Continue reading "A simple scenario simulator for Vanguard optimal portfolio"

The power of diversification and its limits by the example of DAX

Summary

- Sometimes (esp. to fool inexperienced retail investors) the diversification is claimed to be a silver bullet (even in a financial crisis). I show that in crises the diversification effect weakens significantly but still persists (esp. for "defensive" stocks).

- I argue that in a normal (non-turbulent) market the diversification is very helpful in theory but also critically consider its applicability in practice.

- The results that we obtained for the DAX / German stock market should be extrapolated with caution for other markets. You will also see why it is better to watch and know the market (rather than to blindly rely on quantitative analysis and common sense).

Continue reading "The power of diversification and its limits by the example of DAX"